Disclosure: This post may contain affiliate links that earn me a small commission, at no additional cost to you! See our disclaimer for details.

Financial Terminology for Dummies

If you are new to personal finance or are learning financial terms for school, there is a lot of new financial terminology! Flashcards are a great way to remember new financial terminology.

Below are 40 terms that are outlined into four categories: Personal finance, investing, credit and loans, and rental investing.

In this article you will find terminology for personal finance, investing, and rental investing! Be sure to not miss out on downloading your free finance flashcards!

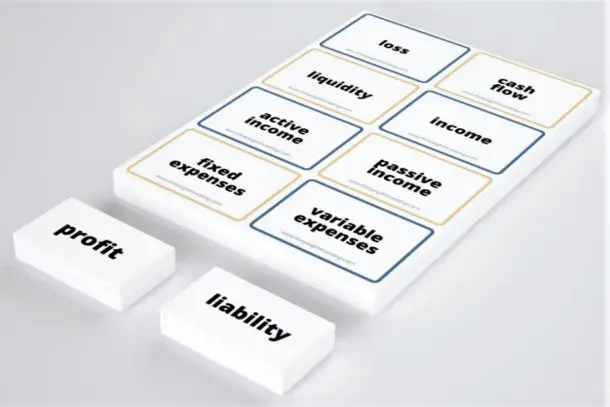

Download your 40 Free Finance Flashcards

Below there are definitions for each of the terms that are provided on the free finance flashcards. However, make sure to print out or bookmark this page alongside with your flashcard printable! This will help you to remember the definitions as you study and learn your financial terminology.

Tip: Print these flashcards out and purchase some laminating paper! You can then keep these flashcards to study finance terms with your children or take them to-go without damaging them!

Personal Finance Terminology

1. Asset

An asset is something you own that will make you money in the future!

Some common assets include: retirement accounts, land, cash, and investment accounts. A “Current Asset” is one that you will be able to liquidate fairly quickly. A “Fixed Asset” won’t be easy to liquidate, or may cost you heavy fees if you do so. Current and fixed assets fit within the “Tangible Asset” It is one that you can see or touch.

2. Liability

A liability is something you own that will take money from you and not make you money in the future.

Some common liabilities include: credit card and student loan debt, homes, boats, and RV’s. A car depreciates in value fast and quickly becomes a liability. A home is commonly referenced as an asset, but there are many reasons why it is actually a liability!

3. Net Worth

Net worth is the amount of money that you are worth. As in, it is the compilation of your assets and liabilities.

Use a free app like Personal Capital to list all of your bank accounts and everything you own. Include all of your debt as well, like your loans and liabilities. Your net worth will either be a positive or a negative number.

4. Debt

Debt is when you owe money back to someone.

When having debt, it means that money was once borrowed, and has not been paid back. Debt can be paid back is various ways and in differing timeframes.

5. Debt Freedom

Debt freedom is when a person has achieved the status of not having any debt to their name.

This status is popular amongst the Debt Free Communities on social media. Debt freedom is the precursor to financial freedom.

6. Financial Freedom

Financial freedom is the status of being able to live without needing to actively work for income.

There are many types and stages of financial freedom that have been created by the F.I.R.E. community. Achieving financial freedom is the ultimate goal of many individuals on a “financial journey”.

7. F.I.R.E.

F.I.R.E. stands for Financial Independence Retire Early. The acronym FI stands for Financial Independence.

8. Profit

A profit is money earned that exceeds money that was spent.

If you spend $20 but earn $30, then your profit is $10.

9. Loss

Loss is money that you lose during a business transaction.

Example: If you spend $20 but only earn $15, then you do not have a profit, and your loss is $5.

10. Cash flow

The concept of cash flow is how money comes in and goes out every month.

There are always things you need to buy and money that you earn. Cash flow is this monthly flow of money, in and out.

11. Liquidity

Liquidity is how easily accessible your money is to “cash out”.

Think of the difference between having an expensive painting and having money in stocks. You can quickly sell your stocks to have money on hand, but it may take awhile to sell a painting if you are in need of cash.

12. Income

Income is money that you earn.

Income can be taxed, or not. There are also many forms of income. Income is essentially an umbrella term for money that you earn.

13. Active Income

Active income is money that you earn from doing one task.

Essentially, active income is earned by doing a job and getting paid for that job. You don’t get paid in the future for jobs you have not accomplished. Most W2 salaried jobs are under the term of active income.

An example of this is lawn mowing. If you mow three lawns then you will earn money from those three lawns. You wouldn’t earn money from six lawns or any money in the future.

14. Passive Income

Passive income works by doing a job today and earning money from it in the future.

This form of income is very popular amongst individuals who seek financial freedom. It allows you to put in effort upfront but earn from those efforts for years.

Popular passive income methods include earning from YouTube, blogging, writing books, and selling digital products.

15. Fixed Expenses

Fixed expenses are expenses that do not change each billing cycle.

For example, you may belong to Netflix, which has a set monthly fee. Your home mortgage, gym membership, or car payments are considered fixed expenses as well.

16. Variable Expenses

Variable expenses are expenses that change each billing cycle.

An example of this is the cost of your food each month, clothing costs each month, or even how much money you spend on Starbucks. It can be difficult determining the cost of these budget items due to their variability.

17. Gross Income

The money that you earn, whether active or passive, initially is your gross income.

The term gross in this context means “overall”. This money is what you get before it is taxed, as in, you do not get to keep all of your earned gross income.

18. Net Income

The money that you keep after taxes are taken from your gross income is considered your net income.

The amount of taxes that are taken out of your paycheck varies depending on if you are a W2 salaried worker, are self-employed, and how you earned the money.

Credit and Loans

19. Loan

A loan is a debt in which the borrower receives an amount of money and is required to pay it back.

There is typically interest associated with a loan and repercussions if the loan is not paid back, ranging from high fees to repossession.

20. Principal

When receiving a loan, the principal is the amount of money originally borrowed.

21. Interest Rate

As a consequence for borrowing money, interest accumulates on a fixed schedule.

Loans have an attached interest rate, which is a percentage of the principal loan amount. Interest rates vary drastically depending on the terms of the loan, and what type of loan it is. You could have one loan with a 2.5% interest rate and other at 25%.

22. Inflation

Inflation is the rise of the prices of goods and services over a period of time.

As inflation causes the rise of prices, the amount of goods and services that currency can purchase is decreased. Your money can buy less things over time.

23. Credit Score

Credit score is a number that reflects a person’s credit history.

Credit scores are calculated based on debt history, payment history, longevity of your debt, and how many credit accounts you have open. An 800 is considered the highest credit score.

24. Credit Report

A credit report is referenced by banks and credit card companies to determine a person’s history of payments, loans, and credit cards.

For example, the data on a credit report helps bankers and lenders determine if a person would be eligible to open another line of credit, or to provide another loan.

25. FICO Score

A FICO score is a type of credit score that evaluates your ability to handle credit.

An open line of credit is a short-term fund with a maximal amount allowed to borrow.

Similar to a credit card, there is interest associated with this type of credit, but only accumulates interest if you borrow the money. Lines of credit can be secured or unsecured.

Investing

27. Individual Retirement Account

An IRA (individual retirement account) is a retirement option that allows Americans to set aside funds for the future.

There are two types of IRAs: Traditional and RothIRA. Anyone can open an IRA on their own, without assistance from a financial planner or financial advisor. There are many financial institutions online that offer IRA accounts.

Learn about the difference between a RothIRA and a Traditional IRA here!

28. 401k

A 401k is an employee-provided retirement option. It is only available to individuals working for specific companies or businesses.

401k’s are an alternative option for saving money for retirement. The downside with these accounts is the hefty tax on withdraws. However, many companies provide what is called a “match”, which means they will place money into your retirement account if you put in a specific amount.

29. Return on Investment

Return on Investment is abbreviated “ROI”. It is the ratio of amount of money that you get back after putting in money for an investment.

ROI is typically seen as a percentage. This number helps you to determine if you got a little, a lot, or even lost money from an investment. The higher the ROI, the better an investment was.

25. Stock

A stock is buying a small ownership of a company.

A stock is also known as a share. People can purchase stocks or shares of a company and can earn small amounts of earnings from those companies, called dividends.

26. Mutual Fund

A mutual fund is essentially a pile of money that is invested in stocks, bonds, and other investments.

The reason it is called a mutual fund is because people mutually provide funds to create a large pool of cash that is collectively invested. These are typically managed by fund managers.

27. ETF

ETF stands for exchange traded fund. An ETF is a type of investment, similar to stocks in how they are sold and traded.

ETFs often are similar to index funds. They are compilations of shares within a specific category, like technology, agriculture, or even ones that are similar to the S&P500.

Rental Investing

28. Landlord and Tenant

A landlord is an individual who owns a property, land, or building.

The tenant is an individual who lives in the property (ex. living in a unit of an apartment) and pays the landlord to reside in the landlord’s property.

For example, if you own a house and rent out a bedroom to a friend, you would be the landlord, and your friend would be the tenant.

Single Family Home

A single family home, commonly abbreviated as “SFH”, is a property where only one family resides in.

These residences are what many people traditionally consider a house. It is a single dwelling where one “main tenant” lives in.

29. Multifamily Homes

A multifamily home has 2 to 4 units, commonly known as duplexes, triplexes, and quadplexes.

As the name suggests, these units house multiple families, all within one attached unit. They are essentially 2-4 separate residences that are connected by the same building.

30. Buy and Hold

The buy-and-hold method of rental investing is the most common way to invest in real estate.

Buy-and-hold real estate involves purchasing a property and renting it out for a number of years, and benefitting from cash flow from the rent to pay down the property.

31. Live in Flip

The live-in-flip method essentially requires you to purchase a home that requires some rehabilitation and is below market value, then to improve the home (flooring, paint, add a bedroom, etc.), then sell the property.

This is a popular method of rental investing because you can avoid paying capital gains taxes on the sale of the property, but you need to have lived in the home for 2 of the previous 5 years.

32. Fixer-Upper

A fixer-upper is a property that requires some level of work before it can realistically (or, safely) be rented out.

The amount of rehab needed to be done on a property varies significantly, with some homes requiring new electrical, to other homes that just need a new paint job.

33. Commercial Real Estate

Commercial real estate involves renting out a space, unit, or building to businesses, rather than families for living.

This can include anything from yoga studios, to doctor offices, to donut shops. Investing in commercial real estate typically costs much more, due to needing a higher down payment, and due to the buildings costing much more than a traditional single family home.

34. BRRRR

The term “BRRRR” stands for: Buy, Rehab, Rent, Refinance, Repeat.

The key to this rental investing method is that all you need is your initial investment! You first buy a good cash-flowing property, fix it up (see: fixer-upper), rent it out, refinance the property with a low interest mortgage, and repeat the process.

During the refinance process you get your money back, in order to have cash to invest in your next property!

35. Turnkey

Turnkey investing involves purchasing a rental property from a company who can find a property, rehab it, and can have it managed by someone else.

You usually can then rent the property out right away, without needing to put extra time and money into fixing it up. Each turnkey company does this process differently, with some requiring you to do more or less effort to get to the point of renting. As in, one company may simply find you properties, while other will get it rent-ready.

36. House Hacking

Using house hacking is the easiest way to begin rental property investing!

The basic definition of house hacking is when your primary residence becomes your investment.

How’s hacking can be done in multiple ways. Below are a few examples:

- Buying a small multifamily property of two to four units in living in one of the units

- Renting out a room in your home

- Purchasing a home with a “mother-in-law suite” and renting out one or both of the units

The reason that house hacking is so popular is because it can significantly decrease your living expenses! Your tenants can essentially pay for your mortgage, allowing you to live for free.

37. The MLS

The MLS stands for “Multiple Listing Service”.

This is essentially the master list of all the homes and properties that are listed by real estate agents. It is the collection of all the listing services, combined.

The MLS is only accessible to real estate agents. Many real estate agents get their license to have access to this ultimate list of active properties! Having the opportunity to use the MLS gives an agents the first access to all homes that are for sale.

Go learn about why I recommend being a real estate agent as an investor!

38. Accountability Partner

An accountability partner is a person who agrees to keep you on track!

When you start anything new, it can be difficult to stick with it! This is especially true when it comes to new habits. You are likely to quit a new habit within the first three months!

An accountability partner can be a close friend, relative, or even your spouse. This person is someone who you can check in with on a regular basis (once a month is sufficient) and this person is someone who can motivate you and help you through the process of staying on track with your goals. If you do not already have an accountability partner, I highly recommend you find someone who can check in with as a rental investor!

39. Neighborhood Class

Neighborhoods are rated on a scale from A to D, and sometimes from A to C, or A to F.

A would be considered top-notch, while D (C, or F, depending on the rating scale) would be the worst condition. Properties can also be considered on the rating scale as well, essentially stating that a home itself can be in a great condition, or in a horrid condition.

Class A locations involve the newest and best. This may be areas of the best schools or high-end retail, for example. They are also more expensive, resulting in less cash flow on your end, if you consider investing in one of these properties. You may consider these areas “upper-middle to upper class”.

Class B locations are considered to be “good” areas, but are not brand new. They typically are safe locations that have amenities and decent schools. You may consider these areas “middle class”.

Class C locations are older neighborhoods. You may consider these areas neighborhoods that are more blue-collar or with workers that have low-wage jobs. Rents are low and homes may require a lot of renovation.

Class D locations are areas that may be considered very dangerous, run-down, or neglected. There typically is crime in the area and many rental investing gurus warn newbie investors to stay clear of these areas due to safety and the significant difficulty of finding and keeping good tenants.

40. Wholesaling

Wholesaling is a unique form of investing using real estate, and is very different than other methods listed above.

Real estate wholesaling consists of finding a property at discount then selling the contract to the property to another individual. The person who would be buying the contract would likely be a rental investor looking to flip or rent out the property.

Summary

There are many terms that are necessary to understand if you are new to personal finance, investing, or real estate!

Be sure to download your free finance flashcards PDF printable to get started learning all of these terms!